.svg)

.svg)

Research Tax Credit Retroactively: Use 4 Years - Deadline 2025

Use Research Tax Credit retroactively: Receive up to 35% reimbursement for R&D costs over 4 years. Check projects 2021 now - deadline end of 2025.

Using the Research Tax Credit Retroactively for Four Years

The Research Tax Credit offers German companies a unique opportunity to claim already completed research and development projects for tax purposes. Since its introduction in 2020, companies can apply retroactively for four years for this government funding, but the deadline for projects from 2021 is expiring soon. Applications for fiscal year 2021 must be submitted by the end of 2025 to secure the full tax relief of up to 35 percent of eligible expenses.

Important Funding Rates and Deadlines at a Glance

Basically, the Research Tax Credit amounts to 25 percent of the eligible assessment base, primarily R&D personnel costs. For small and medium-sized enterprises (SMEs), the funding rate increases to 35 percent for certain periods, so with an assessment base of up to 10 million euros per fiscal year, a maximum funding amount of 3.5 million euros is possible.

The Research Tax Credit can be applied retroactively for up to four years per fiscal year. For expenses from 2021, the application must be submitted by December 31, 2025 at the latest, so that the complete year 2021 can be considered.

From an assessment base of 10 million euros per year, a maximum of 2.5 million euros funding at 25 percent or 3.5 million euros at 35 percent funding rate is realistic.

From kick-off to submitted application with high success chances, companies should realistically plan 1-2 weeks for internal preparation and coordination with consultants. Felsaris supports with full capacity to secure the funding opportunity for 2021 in a timely manner.

Why the Research Tax Credit Is Particularly Valuable for SMEs and Start-ups

The Research Tax Credit is more than just a tax relief. It represents direct financial support that helps companies minimize innovation risks and continuously advance research activities. Especially for small and medium-sized enterprises, which often work with limited resources, this funding can make the crucial difference.

At Felsaris, we have supported numerous companies in recent years in systematically documenting their research activities and evaluating them under funding law. Experience shows: Many innovative projects meet the requirements for the Research Tax Credit without those responsible being aware of it. Particularly in the areas of product development, simulation, and AI-supported optimization, eligible expenses often arise that can be refinanced through the Research Tax Credit.

What Is the Research Tax Credit and How Does It Work?

The Research Tax Credit is a government tax-based funding that offers companies direct financial support for their research and development activities. Unlike classic funding programs such as ZIM, which must be applied for in advance, the Research Tax Credit can be claimed retroactively for R&D projects already carried out.

The mechanism is simple: Companies receive 25 percent of their eligible expenses back as a tax credit; SMEs can use an increased rate of 35 percent for certain periods. This credit is either offset against tax liability or, if there is no sufficient tax liability, paid out directly. From 2024 onwards, up to 10 million euros in eligible expenses can be claimed annually, which corresponds to a maximum funding of 3.5 million euros for SMEs.

The assessment base primarily includes personnel costs for employees who are directly involved in R&D projects, as well as costs for contract research to external service providers. For contract research, typically 70 percent of the contract sum is recognized as eligible, provided the further requirements are met.

Tax-Based Research Funding and Other Instruments

Tax-based research funding through the Research Tax Credit complements existing funding programs and can be used in parallel with them. Unlike project-based funding such as ZIM or BAFA innovation vouchers, the Research Tax Credit is technology-open and sector-independent; it does not require prior approval or project authorization.

This approach makes tax-based research funding particularly attractive for companies that continuously invest in R&D but do not always have the resources for complex application procedures. At the same time, companies that already receive other funding can use the Research Tax Credit for additional, non-funded R&D activities, as long as no double funding of the same expense occurs.

Which Project Periods Are Eligible?

In practice, similar situations repeatedly arise when classifying R&D projects temporally. The Research Tax Credit is designed so that different project periods can be covered, as long as the expenses are assigned to a fiscal year and applied for within the deadlines.

Typical scenarios are:

Project begins and ends in the past (e.g., 2021-2022), here expenses can be claimed retroactively for each affected fiscal year, as long as the application deadlines are met.

The project begins in the past and ends in the future, then the eligible expenses of the fiscal year are distributed over several years.

The project begins and ends in the future, here the funding is regularly made retroactively per completed fiscal year.

For particularly innovative companies, it is also possible to run several independent innovation projects in parallel and submit corresponding Research Tax Credit applications, provided the demarcation of projects and costs is clearly documented.

Correctly Identifying Eligible Projects and Expenses

The definition of eligible R&D activities is based on the OECD's Frascati Manual and includes basic research, industrial research, and experimental development. In practice, this means that all systematic, creative work to expand knowledge or develop new applications is eligible, provided it goes beyond routine improvements.

Particularly relevant for technology-oriented SMEs and start-ups are the following activities:

Systematic experiments to optimize existing products or processes.

Development of new simulation models or the implementation of AI-based solutions, for example in the areas of image recognition, data analysis, or predictive maintenance.

Digitization of one's own product portfolio to position oneself for a highly dynamic, international competition in a future-proof manner.

Development of a machine, a coating methodology, a device, or a technical system with clear structuring into concept phase, design phase with design and simulation, test phase with prototype construction, data analysis, and documentation.

Drastic reconceptualization of one's own product with reduced installation space and weight while simultaneously increasing functionality.

Adaptation of existing technologies to new application areas, such as retrofitting internal combustion engines for hydrogen operation.

The challenge often lies in correctly distinguishing between eligible R&D activities and routine activities. It is crucial that a scientific-technical risk exists and new findings are gained; the mere application of known methods or production according to established procedures is not eligible.

The Three Central Funding Criteria

For a project to be recognized as eligible with high probability, three criteria in particular should be met, which are based on the specifications of the Research Tax Credit Act.

Novelty / high degree of innovation: The work aims to gain new knowledge or new combinations of existing technologies and thus go beyond the state of the art at project start. Ideally, the product, function, or specific combination of features did not yet exist in this form on the market.

Clear technical risk: There is a real technological or scientific risk as to whether the targeted solution can be achieved; even failed solution paths or failed projects are eligible, as this innovation risk is precisely what is rewarded.

Planning: The project is systematically planned and carried out, with clearly defined goals, work packages, milestones, and documentation of the procedure and results.

These three points are particularly carefully examined in the project presentation for the BSFZ and should therefore be clearly worked out in the description and documentation.

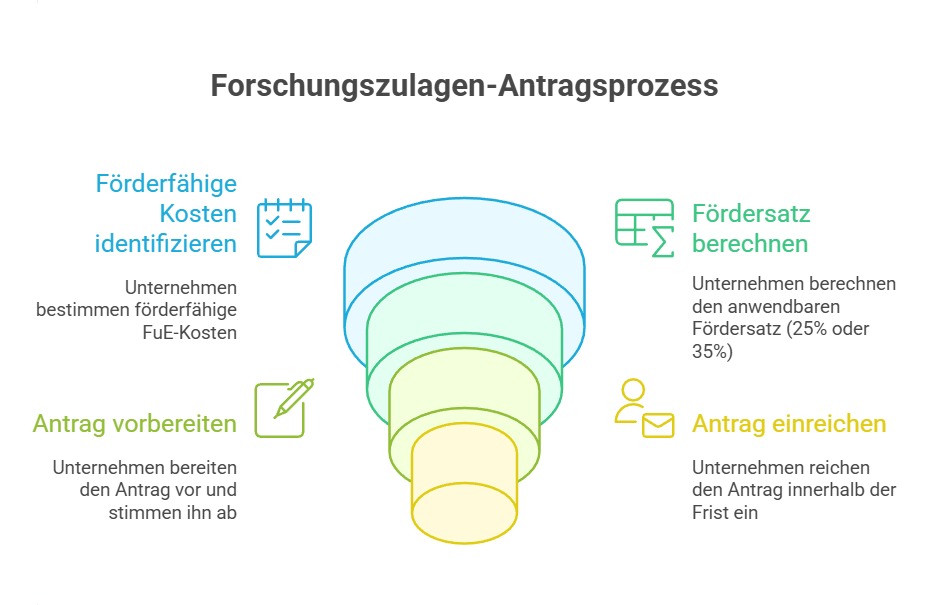

Successfully Mastering the Two-Stage Application Process

The application process for the Research Tax Credit is divided into two stages: First, a certificate about the eligibility of the R&D project must be applied for from the Research Tax Credit Certification Office (BSFZ). Only after receiving this certificate can the actual Research Tax Credit be applied for from the responsible tax office.

The BSFZ examines exclusively the technical suitability of the project. The presentation of the scientific-technical content, the targeted findings, and the degree of innovation is decisive, so that a precise project description is essential for success. The tax office, on the other hand, examines the amount of eligible expenses and determines the Research Tax Credit, for which a clean cost determination and the correct allocation of expenses to R&D activities are decisive.

Observe Retroactive Application and Expiring Deadlines

The possibility of retroactive application makes the Research Tax Credit particularly attractive. Companies can still receive funding up to four years after the end of the respective fiscal year, provided the applications are submitted within the extended deadlines. For fiscal year 2021, this means that applications must be submitted by the end of 2025 at the latest, so that the expenses for 2021 do not expire.

This deadline should not be underestimated, as compiling the required documents and preparing the project documentation often requires more time than planned. Especially with complex development projects or when several R&D projects were running in parallel, careful preparation is essential. Companies should therefore promptly examine which projects from 2021 qualify for funding and initiate the necessary steps early.

Practical Implementation for SMEs and Start-ups

For small and medium-sized enterprises as well as start-ups, applying for the Research Tax Credit brings specific challenges. Often, dedicated resources for application or the know-how for correct project demarcation are lacking, although these companies in particular can benefit especially from the funding.

A systematic approach is therefore recommended:

Identify and document all R&D activities of the relevant fiscal year (project lists, time recordings, cost calculations).

In the second step, check eligibility based on the legal criteria of novelty, technical risk, and planning.

Personnel costs deserve special attention, as they usually make up the largest share of eligible expenses. Important here is the correct proportional allocation of employees to R&D activities, for example through time recording or project controlling. Costs for external service providers or contract research can also contribute significantly to the assessment base, provided the content criteria are met.

Concrete Calculation Example for the Research Tax Credit

To make the dimensions of the funding tangible, a simplified calculation example with only two developers is worthwhile. Assuming two engineers or IT specialists each receive 80,000 euros gross annual salary and are 80 percent engaged in an eligible Research Tax Credit project; in a typical calculation, employer contributions are additionally considered, so that the eligible personnel costs per person can be significantly higher than the gross salary.

Over several fiscal years, this can quickly result in a considerable funding amount. For the period 2021-2023, achievable funding amounts in the range of around 96,000 euros are possible under suitable framework conditions, for 2024 for example about 41,000 euros, and for 2025 around 45,000 euros, so that for 2021 to the end of 2025 a total of about 182,000 euros in funding can result, for work that has already been completed and is now being retroactively honored. The actual amount depends on the detailed personnel costs, the exact R&D workload, and the classification as an SME and should be individually calculated based on real wage and project times.

Optimizing Funding Amount and Combination with Other Instruments

Maximum utilization of the Research Tax Credit requires strategic planning. In addition to correctly recording all eligible expenses, companies should examine the possibilities for combining with other funding instruments.

Basically, the Research Tax Credit can be used in parallel with other funding programs, as long as no double funding occurs. For activities already funded through ZIM, EU programs, or other grants, no additional Research Tax Credit can therefore be applied for, but for additional, previously unfunded R&D expenses. This combination opens up interesting possibilities, for example funding basic development through ZIM and using the Research Tax Credit for further optimization work or customer-specific adaptations.

Fulfilling Documentation and Proof Requirements

Complete documentation is essential for the success of the Research Tax Credit. This begins with the project description and extends to detailed cost recording, as audits often occur with a time delay and retrospective reconstruction can be difficult.

It is recommended to create a project file for each R&D project proving technical objectives, work plan, involved persons and their activities, as well as all relevant costs. Intermediate results and findings should also be documented to prove the R&D character. For cost determination, precision is required: personnel costs must be recorded proportionally and project-related, invoices and performance certificates are required for external services, and material costs can only be claimed if they are directly attributable to the R&D project.

Avoiding Common Mistakes and Increasing Success Rate

In practice, certain errors repeatedly lead to rejections or reductions. A common cause is insufficient presentation of the R&D character, for example when it is not clearly described what new findings are to be gained or what the scientific-technical risk consists of.

Another critical point is correct cost determination. Not infrequently, expenses are claimed that are not directly attributable to R&D activities, or the required evidence or clean temporal allocation of personnel costs is missing. To avoid these pitfalls, early consultation with experts is recommended, who support both with the technical project description and with the allocation of costs under funding law.

Integration into Corporate Strategy

The Research Tax Credit should not be viewed as an isolated funding instrument but as a building block of a comprehensive innovation strategy. Companies that regularly invest in R&D can significantly reduce their innovation costs through systematic use of the Research Tax Credit and create additional resources for further development activities.

Particularly interesting is the combination with other funding instruments and the targeted use of consulting services, for example through BAFA innovation vouchers. Funded consulting projects can thus help identify eligible R&D activities, structure them optimally, and build up internal funding know-how in the long term. For start-ups, the Research Tax Credit also offers the opportunity to benefit flexibly from government support already in the early phase without having to commit early to individual programs.

Conclusion: Act Now and Secure Funding Opportunities

The Research Tax Credit offers German companies an attractive opportunity to have their R&D activities funded by the government; through retroactive application over up to four years, interesting financing opportunities arise even for already completed projects. For projects from 2021, the application deadline ends at the end of 2025; those who want to use the full year 2021 should therefore promptly examine which activities are eligible and prepare the required applications.

Professional consultation can help to fully exploit the potential and avoid common errors in application. The investment in expert support usually pays off many times over: In addition to correct processing, companies benefit from valuable insights for future R&D projects and can optimize their innovation strategy in the long term. Use your chance for up to 35 percent reimbursement of your R&D costs; Felsaris offers a free initial assessment of your projects and supports in securing the funding opportunities for 2021 and subsequent years in the best possible way.

Frequently Asked Questions About the Research Tax Credit

What Types of Companies Can Apply for the Research Tax Credit?

All companies subject to taxation in Germany can apply for the Research Tax Credit, regardless of size, industry, or legal form; what is decisive is that eligible R&D activities are carried out and documented.

Can Already Funded Projects Be Additionally Claimed Through the Research Tax Credit?

No, double funding is not permitted: For expenses already funded through other programs, no further Research Tax Credit can be applied for; however, additional, previously unfunded R&D activities can be considered.

How Long Does the Application Process for the Research Tax Credit Take?

The two-stage process can extend over several months; the BSFZ often requires 3-6 months for technical examination, the tax office then another 3-6 months for determining the allowance. Early, complete application and clear project presentation accelerate the process.

What Happens If the Application Is Rejected?

In case of rejection by the certification office, there is the possibility of objection and subsequent lawsuit before the tax court; however, rejections can often be avoided already through a revised project presentation or supplementary documentation. Expert consultation already before the first application significantly increases the chances of success.

Is the Research Tax Credit Worthwhile Even with Smaller R&D Expenses?

Even with lower R&D costs, the Research Tax Credit can be worthwhile, especially for SMEs with an increased funding rate of 35 percent. Since the application is made retroactively, there are no opportunity costs for non-approved projects, while simultaneously building internal understanding for future funding applications.

How High Can My Research Tax Credit Be at Maximum?

The assessment base for eligible expenses is currently up to 10 million euros per fiscal year; thus, depending on the funding rate, up to 2.5 million euros (25 percent) or 3.5 million euros (35 percent) are possible. The actual funding amount depends on the classification as an SME, the amount of recognized R&D costs, and compliance with state aid limits.

Which Personnel Costs Are Creditable?

Eligible are in particular gross wages and salaries of employees who are active in eligible R&D projects, including employer contributions to social security and other wage-related costs, proportionally according to their actual R&D deployment. The basis is typically payroll statements and time recordings, from which the share of research time in the total work volume can be comprehensibly derived.