.svg)

.svg)

ZIM vs. Research Tax Credit: Decision Guide for SMEs

ZIM vs. Research Tax Credit: Find out which funding fits your innovation project. Clear decision guide for SMEs and start-ups, including combination of both funding programs

ZIM vs. Research Tax Credit: Which Funding Fits Your Innovation Project?

Innovative companies in Germany can choose between various funding instruments to finance their research and development projects. The two most important options are ZIM funding and the tax-based Research Tax Credit. Both programs support technical innovations but differ fundamentally in their structure, requirements, and type of funding. The right choice can determine the success of your innovation project.

What is ZIM Funding?

The Central Innovation Program for SMEs (ZIM) is Germany's most important direct funding program for small and medium-sized enterprises. It supports market-oriented research and development projects with non-repayable grants between 25% and 60% of eligible costs.

Key Features of ZIM Funding

ZIM funding is characterized by its topic-open orientation. Innovative products, processes, and technical services from all industries are funded, provided they demonstrate significant technical progress compared to the state of the art.

Small companies with fewer than 50 employees receive the highest funding rates of up to 40% for individual projects and 55% for cooperation projects. Medium-sized companies with up to 250 employees can expect 35% and 50% funding respectively. For companies in structurally weak regions, the rates increase by an additional 5-10 percentage points.

The maximum eligible project costs amount to €690,000 for individual projects; the project consortium can claim up to €3 million for the entire cooperation project. These sums enable even extensive development projects with multi-year durations.

Eligible Costs in ZIM

ZIM funds project-related personnel costs of scientifically and technically qualified employees who directly participate in research and development. This includes engineers, technicians, and other specialists with appropriate training.

External services such as simulation contracts with engineering firms can be funded up to an equivalent of 100% of personnel costs. This includes development contracts with specialized companies or research institutions as well as testing and inspection services.

Additionally, project-related material costs such as cloud server costs, machinery, or special patent licensing costs are eligible. An overhead allowance of up to 100% covers indirect costs such as rent or machinery depreciation.

What is Research Tax Credit Funding?

The tax-based Research Tax Credit is a relatively new funding instrument that has been available in Germany since 2020. Unlike ZIM, it is a tax-based funding that is granted regardless of company size. Through the Growth Opportunities Act that came into force on March 27, 2024, it has become significantly more attractive, but also more complicated to apply for.

How the Research Tax Credit Works

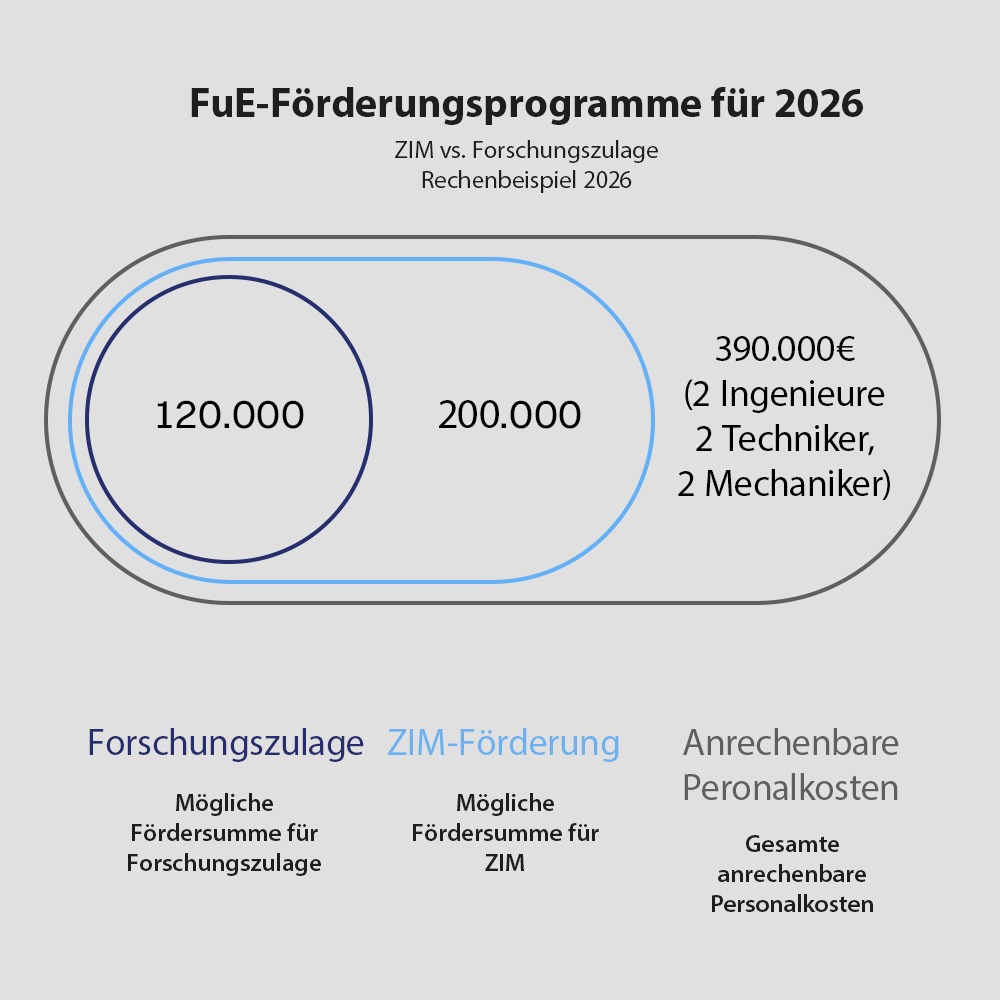

The Research Tax Credit grants a flat tax benefit of 25 to 35% depending on company size on eligible research and development expenditures. This rate range applies equally to all companies, regardless of size or industry.

A maximum of €10 million in eligible expenses can be claimed per fiscal year. This corresponds to a maximum annual Research Tax Credit, i.e., paid funding amount of €2.5 million or €3.5 million for SMEs. Smaller companies benefit from an increased funding rate of 35%.

The application is made retroactively through the BSFZ (Federal Office for Research Tax Credit) of the Federal Ministry of Research, Technology and Space. The application process occurs in 2 stages: The application is submitted and technically reviewed through the BSFZ portal. Once the BSFZ grants approval, in the second step the project costs can be claimed with the tax office with the next annual financial statement. The funding amount is then paid out or offset with the next tax assessment.

Advantages of Tax-Based Funding

The biggest advantage of the Research Tax Credit lies in its predictability and simplicity, and of course that it can be applied for retroactively for 4 years, which is unique for research funding. Companies do not need to submit extensive project applications and can count on the funding with certainty, provided their activities meet the requirements.

The Research Tax Credit is topic-independent and supports both basic research and applied development. Even failed projects are funded, which reduces entrepreneurial risk in innovative ventures.

Particularly advantageous is the retroactive claim. Companies can also have ongoing or already completed projects funded retroactively if the requirements are met.

Research and Development Funding: Direct Comparison

When deciding between ZIM and Research Tax Credit, various factors play a role. ZIM funding is particularly suitable for clearly definable innovation projects with defined market potential.

Funding Volume and Planning Security

ZIM offers higher absolute funding amounts for individual projects. Particularly small companies can expect funding rates of over 50%, which significantly reduces the financing gap for ambitious development projects. Furthermore, ZIM is ideally suited for contacting research institutes to plan an extensive development project. The research institute is funded at 100%.

The Research Tax Credit, on the other hand, scores with planning security. Companies with continuous R&D activities can count on funding year after year without having to go through elaborate application procedures.

Administrative Burden

ZIM requires detailed project planning and extensive application documentation. During the project duration, regular interim and final reports must be prepared. This administrative burden can tie up considerable internal resources at smaller companies. Therefore, at Felsaris we offer the additional package "Project Support & Administration". More at ZIM Funding.

The Research Tax Credit causes significantly less administrative effort. After the initial BSFZ certification, the funding runs through the normal tax procedure. Felsaris supports companies in making this process efficient and avoiding common pitfalls.

Temporal Aspect of Funding

A significant difference lies in the timing of funding allocation. ZIM pays out the grants during the project duration, which relieves the company's liquidity and enables investments in personnel and equipment.

The Research Tax Credit is only granted retroactively with the annual financial statement, typically 1-2 years after completion of research activities. Companies must initially fully pre-finance the development costs.

Innovation Funding for SMEs: Which Projects Are Suitable?

The choice of the right funding instrument depends heavily on the type of innovation project. Both programs have their specific strengths and are suitable for different corporate strategies.

ZIM for Strategic Innovation Projects

ZIM is ideal for companies with clearly defined innovation goals and limited R&D resources. The program is particularly suitable for:

Breakthrough innovations with high technical risk that require an intensive development phase. The high funding rates enable even smaller companies to tackle ambitious projects.

Cooperation projects between companies or with research institutions benefit from increased funding rates and can develop complex technologies that would overwhelm individual companies.

Market entry into new technology fields is supported by ZIM modules for feasibility studies and market launch, with an additional €50,000 in external costs for market introduction that can be funded. These supplementary fundings help minimize risks and exploit market opportunities.

Research Tax Credit for Continuous Innovation

The Research Tax Credit is suitable for companies with established R&D departments and continuous innovation activities. Typical use cases are:

Product development in short cycles, as is common in software development or technical improvements to existing products. The flexible application without clear project delineation is advantageous here.

Basic research and exploratory development benefit from funding even for failed projects. Companies can pursue risk-bearing research approaches without endangering the funding.

Companies with high R&D expenses can optimally utilize the annual €3.5 million maximum funding. Especially in research-intensive industries, the administrative effort pays off quickly.

R&D Funding Germany: Combination Possibilities

An often-overlooked option is the combination of both funding instruments. ZIM and Research Tax Credit do not mutually exclude each other but can be strategically combined.

Sequential Funding

Companies can first use a ZIM project for basic development and then have product optimization funded through the Research Tax Credit. This strategy maximizes funding over the entire innovation cycle.

This approach is particularly worthwhile for long-term development projects. ZIM funding covers the risky initial phase, while the Research Tax Credit supports continuous further development.

Parallel Application

Both programs can be used in parallel for different projects or company divisions. A mechanical engineering company could, for example, have the development of a new product generation funded through ZIM, while ongoing innovative improvements to existing products run through the Research Tax Credit.

However, this strategy requires a clean separation of activities and thoughtful time recording to avoid double funding. In principle, multiple independent innovation projects per year can be applied for and funded simultaneously for both ZIM and the Research Tax Credit.

Funding Program for Companies with Innovation: Practical Decision Support

Criteria for ZIM Funding

SMEs with fewer than 250 employees benefit from the higher funding rates in ZIM. Particularly small companies should examine the possibility of 55% funding for cooperation projects.

Projects with clearly defined innovation goals and foreseeable market potential are ideal for ZIM. The funding requires technical progress compared to the state of the art, which requires a certain novelty.

Companies with limited internal R&D resources can involve external service providers through ZIM and thus temporarily expand their development capacities.

Arguments for the Research Tax Credit

Larger mid-sized companies from 250 employees receive lower funding rates with ZIM, while the Research Tax Credit grants 25% regardless of company size.

Companies with continuous R&D activities and established development processes benefit from the uncomplicated processing of the Research Tax Credit.

Projects with uncertain outcomes or exploratory character are better suited for the Research Tax Credit, as even failed projects are funded.

Consultation by Experts

The optimal funding strategy depends on many individual factors. Our experts analyze your innovation project, evaluate the success prospects of various funding instruments, and take over the complete application and administrative project support upon request. We work on a success-based model for both ZIM and the Research Tax Credit - you only pay for approved applications.

For the Research Tax Credit, we offer comprehensive consultation on the certifiability of your R&D activities and support with the BSFZ application.

Conclusion: The Right Funding for Your Innovation Success

The decision between ZIM funding and Research Tax Credit cannot be answered universally. Both programs have their justification and are suitable for different innovation strategies.

ZIM convinces with high funding rates and direct liquidity assistance but requires considerable administrative effort. The Research Tax Credit scores with simplicity and predictability but offers lower funding rates and delayed payout.

For most innovative SMEs, a combination of both instruments is optimal. ZIM for strategic breakthrough projects, the Research Tax Credit for continuous development activities.

Let us develop the optimal funding strategy for your company together. Contact Felsaris for a free initial consultation and maximize your innovation funding.

Frequently Asked Questions

Can ZIM and Research Tax Credit Be Applied for Simultaneously?

Yes, both programs can be used in parallel, but not for the same activities. A clean separation of funded activities is required to avoid double funding. Felsaris supports with correct allocation.

Which Funding Is Suitable for Start-ups?

For start-ups, ZIM is usually the better choice, as the high funding rates of up to 60% for international cooperations close the financing gap. For particularly risky and innovative projects, funding rates of 70% are also possible through the ZIM feasibility study. Feel free to contact us with questions. The direct payout also improves the often tight liquidity situation of young companies.

How Long Does Approval Take for ZIM vs. Research Tax Credit?

ZIM applications are decided within 3 months. We offer an express package in which we prioritize your innovation within one month from the initial meeting to the completed application. ZIM Funding. The Research Tax Credit is certified by the BSFZ within 1-3 months after application. The tax refund then occurs through the tax office as part of the normal tax return.

What Documentation Is Required for Both Fundings?

ZIM requires detailed project reports, time records, and proof of use. For the Research Tax Credit, structured records of R&D activities suffice, as well as completed time sheets and proper cost recording. Both programs require seamless documentation.

With us, experienced engineers and scientists from practice actively support application preparation as well as the elaboration of innovation content and work packages - a decisive quality advantage, as we specialize exclusively in innovation funding such as the ZIM program and the Research Tax Credit.

By the way: The Research Tax Credit can be applied for not only retroactively but also for future projects. For more complex projects, we are happy to support you personally.